One of the best CEOs I have been honored to work for was Clarke Johnson, then CEO of McGregor Sports in the early 1990s. He told me while we were discussing strategy back then that the hardest part of his job was to tell his people “no”. I was perplexed and asked for more insight. That insight and those of others are the topic of this article.

I define the leadership of strategy as “The customized process to make sure unwanted diversions to a previously successful strategy are noticed and thwarted”. Once your firm’s strategy is formulated and you have started implementing it using your plan as a roadmap, the leadership of strategy takes over. So from my view, the leadership of strategy is different than the popular emphasis on “strategy execution”. From my perspective, execution deals with the timely implementation of the initiatives and projects that will make the strategy and strategic plan a reality. I wrote a book titled The New Science of Strategy Execution in 2004 if anyone desires further background. There were also numerous books and articles published on strategy execution after 2004 one can read. And you might be asking what I mean by a competitive strategy in the first place. Please see other articles in this series on this topic if you desire my take on what a competitive strategy is.

The leadership of strategy has not been discussed very much and it involves guiding and shepherding the strategy through all the stuff that hits your inbox every day, all the hair-brained ideas that come up at the Monday morning staff meetings, all the things your peers tell you that you ought to be doing. Add to this mix the advice from your legal counsel, your board of directors, your bankers, your consultants if you use them and maybe even your spouse, and you can understand what I am trying to say. There are myriad forces everywhere which can try to divert you from your formulated strategy.

Why would Clarke Johnson say what he did above?

My understanding of what was behind Clarke’s statement is the uber-achievement orientation of work in the United States. We are raised by and large to be go-getters and to strive for higher benchmarks. Everyone wants to improve individually and be rewarded for it, no matter how much of a team player they are. So we seem to have a built-in impetus for suggesting new things to do. And if a firm is good at new opportunity recognition, ideas bubble up everywhere. So there are lots of opportunities to “say no”.

But the established firm makes its bets via its current strategic plan and then it must work those bets to reap mid-term returns. Everyone understands that cash flow is the lifeblood of a company. However, unless a CEO and his or her top management team constantly monitor, guide and lead the strategy, it has a huge chance of being diverted by many incremental projects that seem good on the face of it but can actually cause the firm harm, or at least headaches.

“Wait a minute”, you might say if you have been a reader of this column. “Last year you wrote about innovation and how firms that stick with their current offerings for too long and are not innovating have a huge chance of failing outright or merging out of existence”. True I did write that. In fact, I used Whirlpool’s Gladiator Garage Works as an example of “good” innovation. But the truth is, the very powerful brand managers at Whirlpool found this a nuisance. The Gladiator innovation team found that the garage was usually just a door away from Whirlpool’s bread and butter – the laundry room. What seemed like a no-brainer extension did not fit into the painstakingly crafted brand messages of Whirlpool’s key brands. Gladiator Garage Works was launched and it is successful, but only after some churn and gnashing of teeth. If a firm is not careful, all of the weekly new ideas can dislodge a for-profit firm from its distinctive strategy. Firms can morph from being a low-cost provider to something else and can morph from a differentiator to something else. A good process for the leadership of strategy prevents this. And so does the courage to say “no”.

Thus there is a huge balancing act of getting ROIC (return on invested capital) from your current strategy, offerings and roadmap versus milking the current strategy and roadmap too long and not changing by innovating versus changing too frequently via some form of innovation or some form of foolishness. Sometimes the frequent change is caused by the “fad of the month” syndrome, and this is usually toxic. In my experience, the balance is never perfect. Emphasis will sway to one side before it becomes apparent something is out of balance. But what if there was a way to have a good balance most of the time?

This is the stuff of the leadership of strategy and as I mention above it is not talked or written about very much. The leadership of strategy is not a difficult skill set to learn in my view. But the awareness of the need for it amidst all of the things CEOs are told they need to be aware of can make it one of those “hiding in plain sight” kinds of things. A good process for the leadership of strategy requires a daily and weekly drumbeat of things that remind the CEO that the strategy is becoming to be “un-led” and thus may be heading for an out of control situation. This in my view is one of the reasons why good CEOs are worth every penny the board has agreed to pay them – they know how to manage this balancing act through time and not de-motivate key people in the firm.

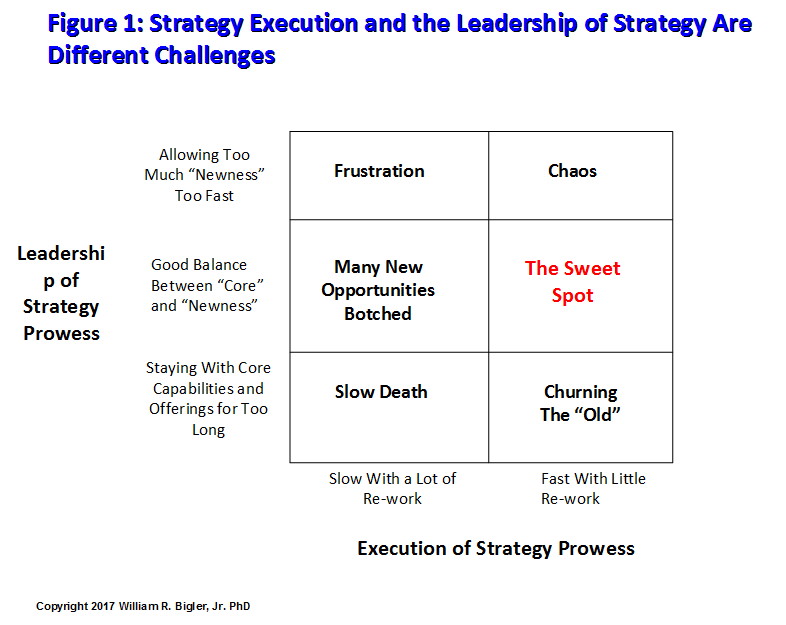

Figure 1 tries to depict some of the many trade-offs and dynamics among staying with “core” products and services for too long versus too frequent and too fast innovation. The reader will hopefully see my view that the leadership of strategy and strategy execution prowess are related but different.

So what is a way to achieve a good balance between sticking to the plan’s roadmap and allowing new ideas to be entertained? In my experience and backed by some practical academic research, a bold approach could be something like the following. It is one of many approaches firms could use:

- Make an indisputable policy that you will obsolete your products and/or services before your competitors do this for you. WL Gore Company has the policy that 30% of its annual revenue must come from new products and services introduced that year. Your percentage could be lower or higher depending on your firm’s situation. This means some products and services need to be harvested on their way out to be discontinued. An innovation process that has a lot in the pipeline is required for this.

- Instead of unbridled innovation all of the time, put a “governor” on your innovation by issuing Guidelines at the beginning of any year’s planning cycle. These Guidelines one year could be very narrow, like “We will only entertain revenue opportunities this year that have a minimum of $X million in revenue potential and that are expected to earn our weighted average cost of capital”. Other years the Guidelines could be “loosened” up to guide the finding of smaller opportunities.

- Develop an appropriate incentive compensation system to reward those people who help find the opportunities within the stated Guidelines.

- Measure the cash flow from each current product and service or groups of like products and services if you can. The first time cash flow falls by x% (you set this policy) from the previous year, either fix the cash flow issue within three months or announce that product or service will be harvested and then discontinued. Sometimes having a commitment to spare parts or something like spare parts prevents this, but it can be done most of the time.

These kind bold solutions are the essence of the leadership of strategy and every firm must find its unique approach that works. Otherwise your previously successful competitive strategy has a good chance to be de-railed.

This article is part of a series on what are the causes of increases in firm valuation for the for-profit firm.

Dr. William Bigler is the founder and CEO of Bill Bigler Associates. He is a former Associate Professor of Strategy and the former MBA Program Director at Louisiana State University at Shreveport. He was the President of the Board of the Association for Strategic Planning in 2012 and served on the Board of Advisors for Nitro Security Inc. from 2003-2005. He has worked in the strategy departments of PricewaterhouseCoopers, the Hay Group, Ernst & Young and the Thomas Group. He can be reached at bill@billbigler.com or www.billbigler.com.