I am asked from time to time how many business people are really strategic in their thoughts and actions. This article will cover the thought part. In my estimation, a relatively few people in business are good strategic thinkers – I think about twenty percent. I am not trying to be inflammatory – only reporting my observations, which could be based on the sample of only the people with whom I have dealt over the last forty years in the field.

Why would you want to develop or improve thinking like a valuable strategist? Notice I use the adjective valuable. There are many charlatans out there and we do not want to learn about or improve upon what they think and do.

Let me build my short argument of why I think improved strategic thinking prowess is important for for-profit firms. Dr. Michael Porter, the most well-known and respected strategy academic in the world, has estimated that forty percent of a for-profit firm’s Return on Invested Capital (ROIC) is determined by the nature of the five competitive forces in a firm’s industry structure. Now industry structure issues are part of the mind of the strategist, but this forty percent is fixed and determined once the strategist has made the decision to compete in a given industry or competitive space. Also, industry structure changes over a long period of time and thus does not have that much opportunity for many rounds of strategic thinking. The other sixty percent of ROIC is explained by the thinking and actions that the particular firm’s people employ. Of that sixty percent, I estimate that a firm’s processes, its infrastructure and its excellence at operations determine thirty percent. So only thirty percent of ROIC in a given firm is caused or determined by what we can call the mind of the strategist. So what is the big deal?

Well, thirty percent is actually a lot and can mean the difference between a mediocre performer and a top performer. In some cases, faulty strategic thinking can doom a firm to downward performance until it fails or merges out of existence.

The rest of this article will chronicle what has taken me almost forty years of practice, on top of great education in the field of strategy, to develop. If you aspire to be a CEO or be a very valuable employee who can aid your firm’s development, this short article can help I think. I will end this article with the “two-minute” challenge so you can assess your current acumen in strategic thinking.

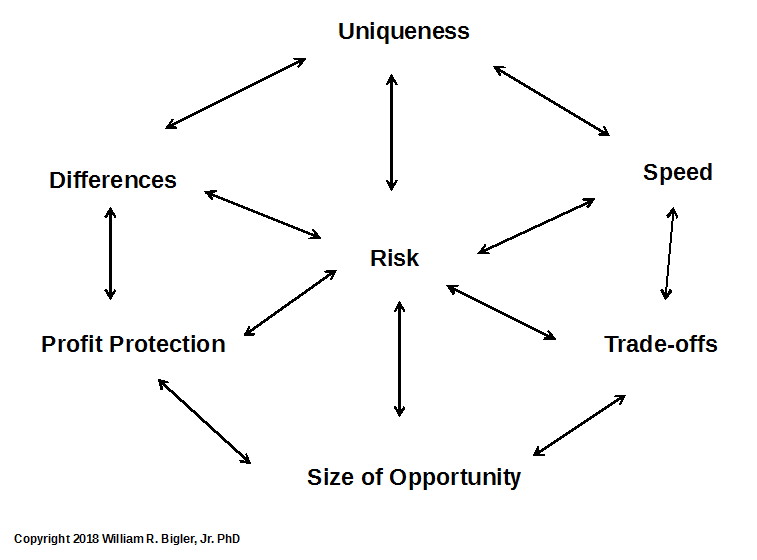

Figure 1 depicts the seven elements that make up the mind of a valuable strategist from my viewpoint. These seven elements have worked well for me and are based on some academic underpinning but mostly come from much experience in the field. They are at a high level of generality as each nests hundreds of different things that could be discussed. As a reminder in ‘sticky strategic thinking opportunities’ I have printed and laminated a card I keep in my briefcase. Notice also the elements are not numbered. They are all equally important and fit together as a united, dynamic system of thinking. Each informs the other and thus the two-way arrows are everywhere in the diagram. This is a reason why good strategic thinking can be so difficult. The mind needs to take in all seven elements at once and then if one element changes in your thinking, there can be an immediate ripple effect change to the other six.

Figure 1: Seven Elements of the Mind of a Valuable Strategist

Uniqueness – Are the competitive strategy and most of its initiatives unique relative to current rivals and expected newcomers? I am considering buying one or two franchises at the time of this writing, however, none excite me, as few are unique. A franchise to organize someone’s shoes in a closet is no different than the many others that purport to do the same. Part of uniqueness for me is to ask and answer this question: Is the strategy or initiative a “nice-to-have” or “have- to-have” proposition? Now nice-to-haves can turn into have-to-haves, as the first Apple iPhone did, but we would like to have “have to haves”. By the way, there is a third option in this element: Is the strategy or initiative a “dumb idea”? There are no dumb questions but there can be dumb business ideas. I know I have come up with a few. Sometimes dumb ideas are simply ahead of their time, but for the most part we ask this person to go back to the drawing board and no longer consider the idea.

Differences – Do the current competitors employ successfully different business models, different company value chains, different branding, different cultures, etc.? More differences make it easier for any incumbent to forge a unique value proposition, business model and supply chain. This is my problem with car dealerships. Not many differences here as one looks pretty much the same as all others.

Profit Protection – Can the firm’s profits be protected from decline for as long as possible into the future? Warren Buffett refers to this as a firm’s “economic moat” and it is one of his key criteria for investing in firms. Many people think of a firm’s ability to secure patents and trade secrets is the key means to protect profits. But this can be transgressed so the firm needs more enduring forms of profit protection. An example would be a unique set of processes and a unique culture in the firm’s R&D group. This can be difficult for any rival to copy in the short to mid-term.

Size of Opportunity – This is both the size of a given opportunity and the size of the current market. A brilliant idea that will have a sixty percent market share of a 500 unit market is not nearly as good as a three percent market share in a three million unit market.

Speed – By this, I mean both the time to gain market traction for the strategy and the time to secure adequate cash flow. A strategy or an initiative that will take more than five to seven years to mature is not good. Now it took Nestle thirty years to gain market traction and cash flow for its Nespresso machine, but this is a rarity.

Trade-offs – Does the strategy require the firm to make critical trade-off decisions? Specifically what things will we absolutely not do? We know a strategy cannot be all things to all people, but many firms ignore this. We want a strategic context that forces us to make decisions on what we will absolutely not do, as most competitors will not make these trade-offs. They usually become cumbersome and too complex. And some firms say they are serious about trade-offs, only to have a salesperson make a one-off request that begins to push the firm into being all things to all people.

Risk – This element is straightforward. It is placed in the middle of the exhibit to simply portray that the other six elements affect actual risk after the strategy or initiative has been put into play. In addition, the expected risk of the strategy or initiative before they are put into play influences perceptions of the other six elements. Notice over time as more information comes to be known, perceived and actual risk can change.

Let me give you a quick case example to practice using these elements. A friend of mine and his wife have developed an all-purpose tool for nurses. The tool has fifteen features and twenty-five applications. They both have been nurses for twenty years and this product was born out of their frustration using multiple tools, some of which were suboptimal, to serve their patients. What would you ask of this venture using the above seven elements?

Here is the two-minute challenge: If after hearing my friend and his wife’s investment pitch, could you size up the opportunity in two minutes as to whether this will be a likely success? Of course, more due diligence is required for investment. However, if you can’t make a judgment about the likely success of a strategy or initiative in no more than two minutes after hearing a typical investment pitch, you need more practice. This framework in Figure 1 has worked for me. What would you add or subtract?

This article is part of a series on what causes a firm’s value to increase.

Dr. William Bigler is the founder and CEO of Bill Bigler Associates. He is a former Associate Professor of Strategy and the former MBA Program Director at Louisiana State University at Shreveport. He was the President of the Board of the Association for Strategic Planning in 2012 and served on the Board of Advisors for Nitro Security Inc. from 2003-2005. He has worked in the strategy departments of PricewaterhouseCoopers, the Hay Group, Ernst & Young and the Thomas Group. He can be reached at bill@billbigler.com or www.billbigler.com.