I have re-written this article five times in the last five weeks (today is March 25, 2020). As we all know the COVDID-19 pandemic has caused huge losses in the stock market. It makes one wonder how stocks are really valued for publicly traded firms and how non-publicly traded firms (think of your favorite family-owned for-profit business) are valued.

Surprisingly, recent studies have shown many executives and board members do not know the basics of valuation creation and the growth of that valuation for their firms. I find this hard to believe with all of the MBAs who have graduated over the last thirty years. But evidently this statement is true or has some truth to it. I have written a few articles here about this topic in particular and indeed the topic of valuation for for-profit firms is the topic of my entire series of articles, numbering at about 75 on March 25, 2020, and started four years ago.

This article follows from my last article titled The Full Potential of Your Business, Performance and Your Firm’s Valuation – Why This Is Such a Powerful Lens On Your Business (click here if interested). In this article, I will present my Causal Model of firm valuation as a series of panels or “Waves” with as little description as possible. It will present though some of my key findings and observations over the years.

The previous article in the link above discussed the private equity (PE) concept of the Full Potential of Your Business (FPOYB). I tried to argue this is an exciting and value-added way to view the performance of your firm and its potential to grow its valuation. I also posited that growing a for-profit firm’s valuation should be the key superordinate goal.

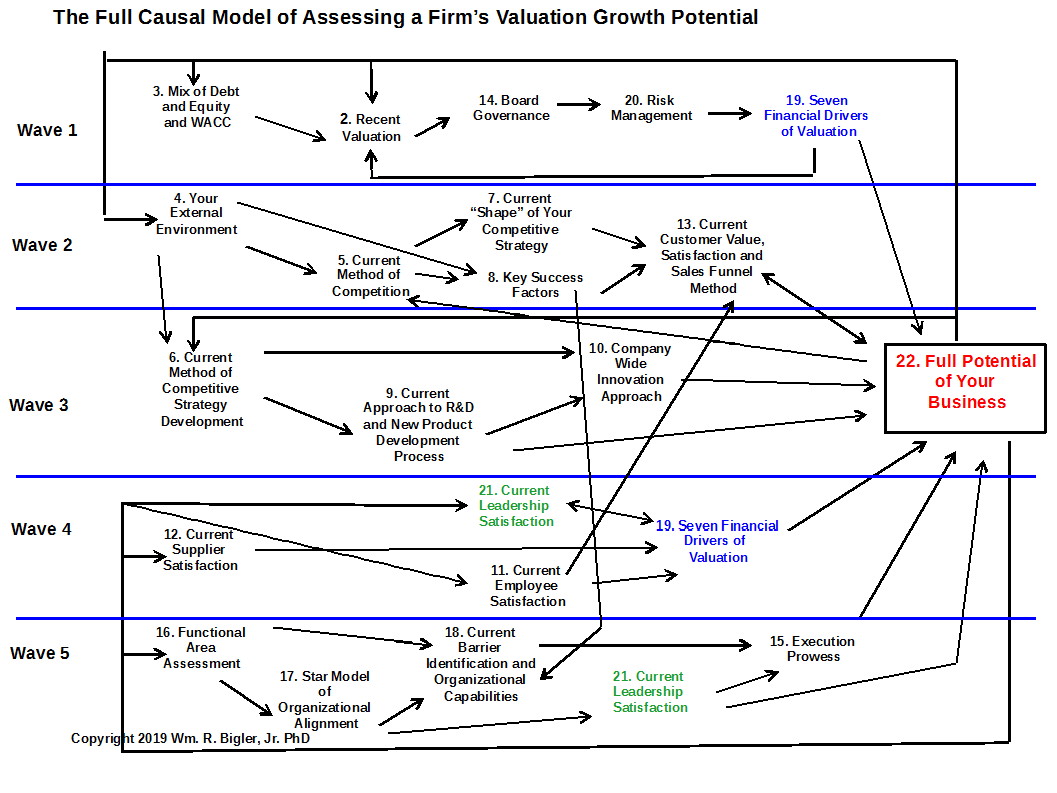

My Causal Model presented below is detailed but includes what I feel are the “necessary and sufficient elements” to describe and explain the causality of firms trying to create and grow their valuation. The Causal Model will build in five Panels or Waves and the sixth will combine them in one comprehensive model. Make sure you are sitting down with a cup of coffee or preferably an adult beverage if you imbibe before perusing the comprehensive model. It is comprehensive and scary looking but simply combines the Five Waves. The model derives from some practical academic research done by me in my intermittent stints as an academic over the years in the field of competitive strategy. But it mostly derives from my almost 30 years in the field of witnessing what works to grow a for-profit firm’s valuation.

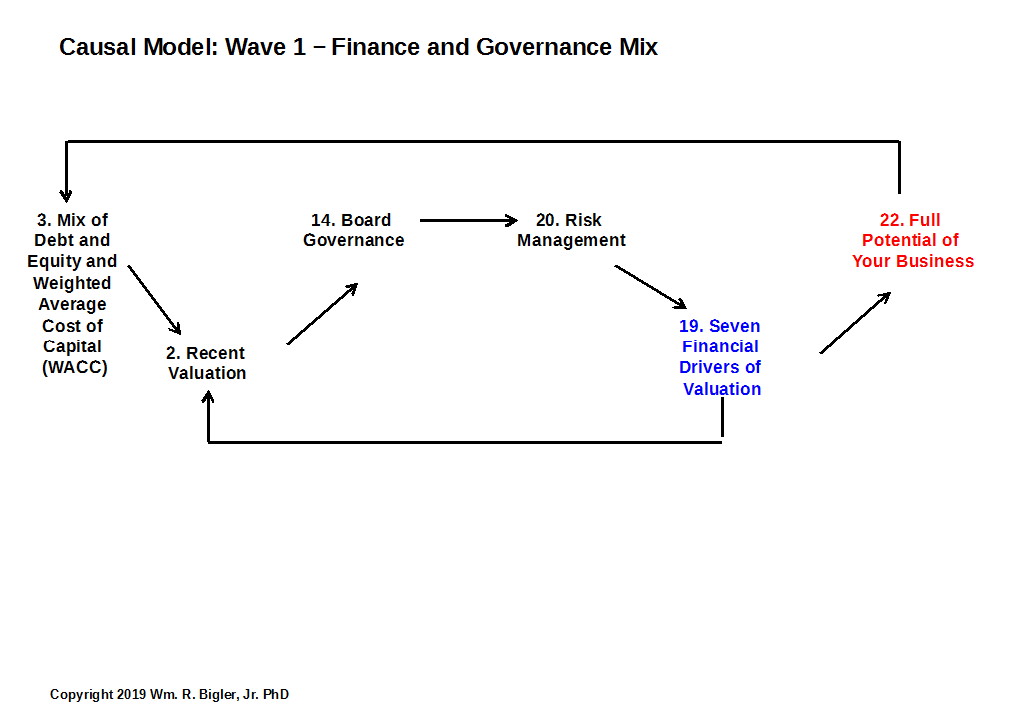

Wave 1: Finance and Governance Mix

The WACC is a key benchmark number. Firms who earn Free Cash Flow Return on Investment greater than their WACC grow company valuation. This is the only way valuation and (and stock prices) can be created and grown.

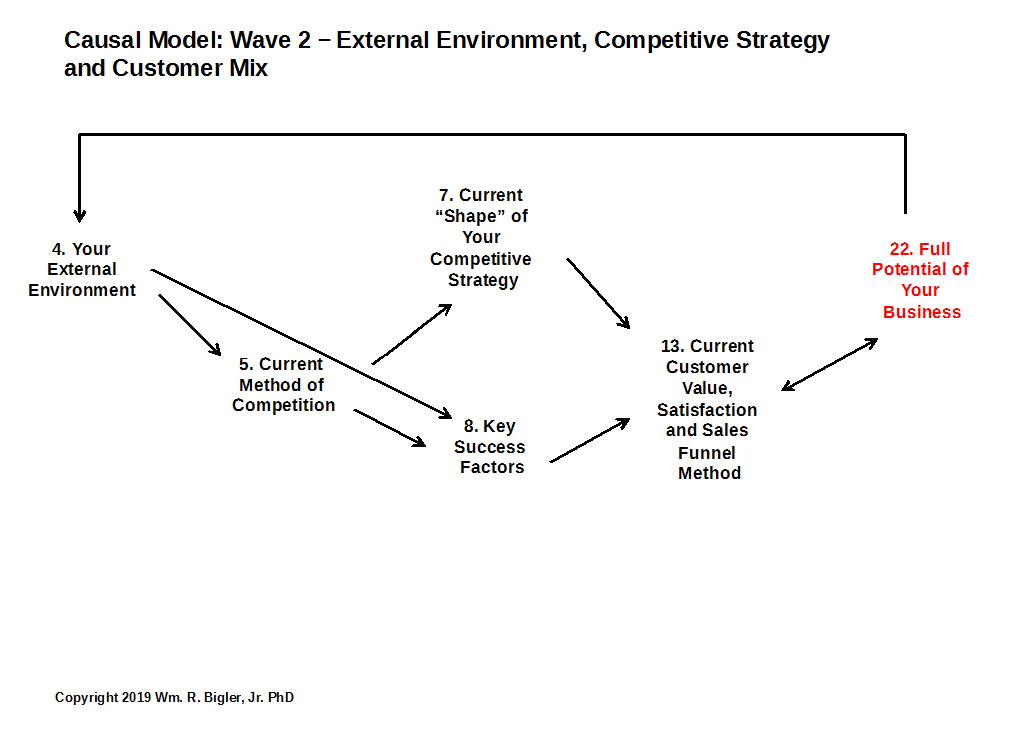

Wave 2: External Environment, Competitive Strategy and Customer Mix

This Wave combines stuff external to your firm and your firm’s response to it. Notice element #22 Full Potential of Your Business (FPOYB) will be in all five Waves and the final comprehensive model.

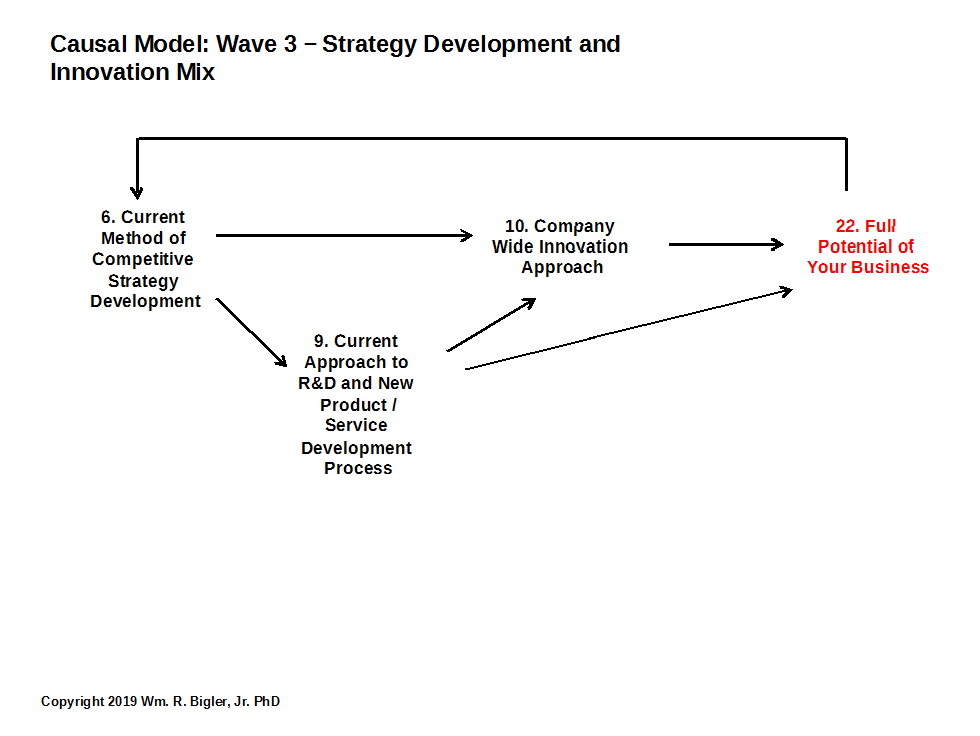

Wave 3: Strategy Development and Innovation Mix

This Wave is heavy on Process to get competitive strategy and the “newness” from R&D and innovation seeded before the variety of initiatives are implemented.

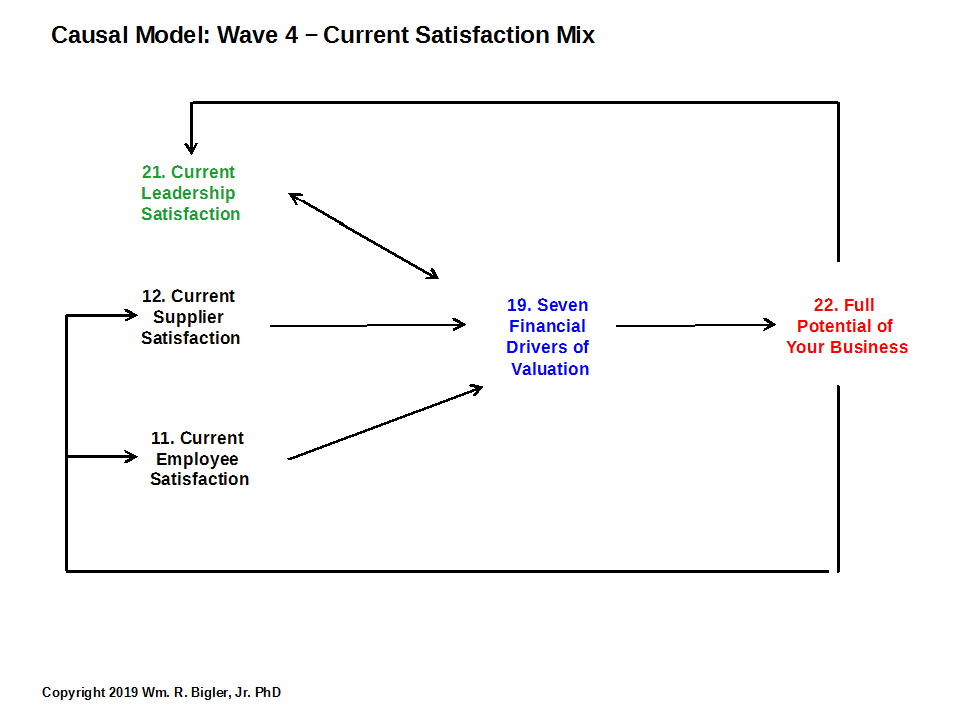

Wave 4: Current Satisfaction Mix

This is a Wave that combines perhaps unusual bedfellows. This Wave measures the current “temperature” of satisfaction among three key groups and their alignment with the Seven Financial Drivers and the FPOYB.

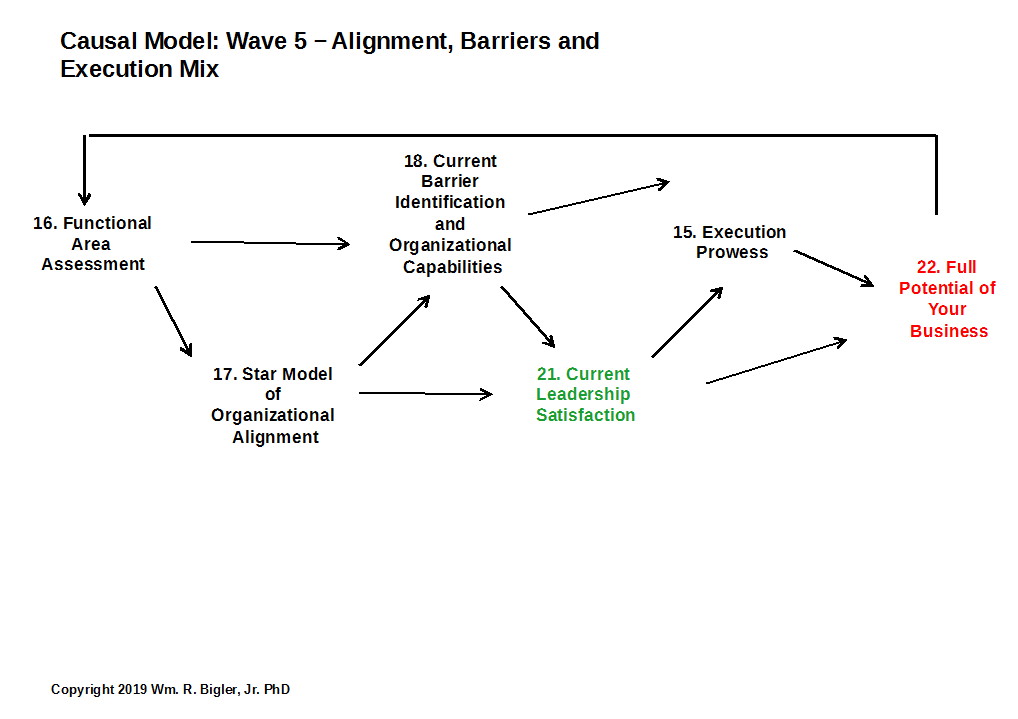

Wave 5: Alignment, Barriers and Execution Mix

Pretty self-explanatory. But notice Current Leadership Satisfaction surfaces again. We normally think with senior leadership being paid handsome sums we would take their satisfaction for granted. My experience shows if good senior leaders get bored or turned off they will leave if they can. For those who should stay we want them to stay.

Drum roll………. the full Causal Model:

Waves 1 – 5: Full Causal Model:

Well if you have lasted reading this article and perusing the Waves for this long thank you. This model has worked for me and I hope you find it useful if not valuable. Notice I have included some linkages between and among Waves. At this stage in my research and practice, all I can say is these Elements are correlated. That is they move up or down together and it is too early to tell what causes what. I hope to rectify this is my ongoing research and work with firms.

But I want to comment on the valuation (covered in Element #2 of the model) we have seen in the stock market over the last five weeks. While it seems to not make sense it does – sort of. A brief review:

- A firm’s current stock price or the valuation of a private, non-traded for-profit firm is the five-year forecasted free cash flow from operations “discounted” to the current time period to reflect the time value of money.

- The valuation measures are reflected in Elements #2, 3 and 19 of my model. These are “End Result” measures. All of the other Elements in the Causal Model are the “Means” to those end result measures.

In times of upward trends in valuation (like just five weeks ago), we see that all of the “Means” Elements and all of the “End Results” Elements seem to be important. But in down markets, all that seems to be important are the “End Result” Elements.

Let me give an example. Value creating firms like Amazon, Home Depot, Apple and others had the same Resources and Capabilities in their firms when the stock market declined rapidly. These did not go away in the mere five weeks when the stock market went from an all-time high to almost an all-time low. So why has the huge drop in stock prices occurred? What happened?

We all know of the spiraling ripple effects that have happened. Demand plummeted, workers were laid off, and supplies were not ordered thus disrupting the supply chain and negatively impacting suppliers. This is the tip of the iceberg for the spiraling effects. This has caused the forecasted five-year free cash flow of firms to fall, thus the decline in the stock prices. So are the financial “End Result” Elements and measures all there is to valuation? What about the productive configuration of Resources and Capabilities? Should these not provide at least a floor to which stock prices will not fall through? Maybe this has happened but I am not sure.

A great test to my model is that when COVID19 is brought under control if the firms have not gutted their ‘Means’ Elements too drastically, we should see their stock prices (and valuations for non-publicly traded firms) beginning to rise quickly. Today is March 25, 2020. I am anxious to see if this proposition will be correct.

Thanks for reading and commenting if you have the interest and the time.

We offer a free Diagnostic Survey using the twenty-two Elements of our Causal Model. The survey is administered anonymously using Survey Monkey. To lessen the time to take the survey by participants we use a process to select up to thirty people in your firm over which to spread the work. Thus the time for any one participant is from four to thirty minutes. The survey is held open for two weeks to allow people to save their work and come back to it. The output are a series of exhibits based on your scores that depict how much potential your firm has now to grow its valuation as it moves to its Full Potential. And it portrays exhibits which suggest how to improve from you baseline situation. During this downtime of being quarantined it might be good time for your firm to do this. If interested please contact Bill Bigler below.

This article is part of a series on what causes a firm’s value to increase.

Dr. William Bigler is the founder and CEO of Bill Bigler Associates. He is a former Associate Professor of Strategy and the former MBA Program Director at Louisiana State University at Shreveport. He was the President of the Board of the Association for Strategic Planning in 2012 and served on the Board of Advisors for Nitro Security Inc. from 2003-2005. He is the author of the 2004 book “The New Science of Strategy Execution: How Established Firms Become Fast, Sleek Wealth Creators”. He has worked in the strategy departments of PricewaterhouseCoopers, the Hay Group, Ernst & Young and the Thomas Group among several others. He can be reached at bill@billbigler.com or www.billbigler.com.